As digital payments continue to dominate global commerce, organizations that process, store, or transmit payment card data face increasing cybersecurity risks. From sophisticated data breaches to payment skimming attacks, hackers constantly target cardholder information. To mitigate these risks and establish a unified security baseline, the Payment Card Industry Data Security Standard (PCI DSS) was developed. PCI DSS compliance provides a globally recognized framework designed to protect cardholder data and strengthen the security posture of organizations involved in payment processing. This blog explores the technical structure of PCI DSS, its core requirements, and how organizations can implement the framework effectively to secure payment environments.

Table of Contents

Understanding the Global Governance of PCI DSS Compliance

The PCI Security Standards Council, founded by major card brands including Visa, Mastercard, American Express, Discover, and JCB, manages PCI compliance.

The council develops and maintains the PCI DSS standard, but enforcement happens through the payment card ecosystem, which includes:

- Card brands (Visa, Mastercard, etc.)

- Acquiring banks

- Payment processors

- Merchants

- Service providers

This structure makes PCI DSS globally enforceable through contractual obligations, rather than through a single government law.

For example, when a merchant signs an agreement with a bank to accept card payments, the contract typically includes a clause requiring PCI DSS compliance. If the merchant fails to comply and a breach occurs, the organization may face:

- Non-compliance penalties

- Forensic audit costs

- Increased transaction fees

- Liability for fraud losses

- Possible termination of card payment services

This contractual enforcement model makes PCI DSS a globally accepted payment security framework.

Get in!

Join our weekly newsletter and stay updated

Gist on PCI DSS 4.1

The latest version of PCI DSs 4.1, brings enhanced clarity, flexibility, and alignment with the evolving cyber security landscape. It emphasis a risk based approach, allowing organziations to tailor security controls to their environments. With stronger authentication requirements and improved implementation guidance, it enables businesses to adopt modern technologies while building more adaptive, scalable, and resilient protection for payment card data.

Additionally, the update refines existing requirements to reduce ambiguity and improve consistency in assessments. It encourages continuous security practices rather than periodic compliance, helping organizations stay proactive against emerging threats. PCI DSS v4.1 also supports customized approaches, giving businesses greater flexibility in how they achieve compliance objectives. Enhanced focus on multi-factor authentication and security testing further strengthens defense mechanisms. Overall, it empowers organizations to align compliance efforts with real-world security needs while maintaining robust protection of sensitive payment information.

Why is PCI DSS Compliance Important for Global Payment Security?

The global payment ecosystem connects merchants, customers, banks, payment processors, and service providers across multiple countries. Payment transactions often pass through several systems and networks before being completed. If security controls are weak at any stage of this process, hackers can exploit those vulnerabilities to steal cardholder data.

PCI DSS compliance plays a crucial role in addressing these risks by establishing a standardized security framework used worldwide. It ensures that organizations handling payment card data follow consistent security practices to protect sensitive financial information and maintain the integrity of global payment systems.

Below are some key reasons why PCI DSS compliance is essential for global payment security.

- Protection of Sensitive Cardholder Data

PCI DSS compliance requires organizations to implement strong security controls such as encryption, access restrictions, and secure storage mechanisms. These measures ensure that sensitive information like card numbers, expiration dates, and CVV codes is protected from unauthorized access.

- Standardized Security Framework Worldwide

One of the biggest advantages of PCI DSS compliance is that it provides a globally accepted set of security standards. Organizations across different countries follow the same framework when processing payment data, ensuring consistent protection of cardholder information regardless of geographic location.

- Reduction in Payment Fraud

By implementing controls such as strong authentication, network segmentation, and continuous monitoring, PCI DSS compliance helps reduce the risk of payment fraud. These measures make it more difficult for attackers to access payment systems or misuse stolen card data.

- Improved Monitoring and Threat Detection

The framework requires organizations to continuously monitor system activity, maintain detailed logs, and regularly test security controls. These practices help security teams quickly detect suspicious activities and respond to potential threats before they escalate into major breaches.

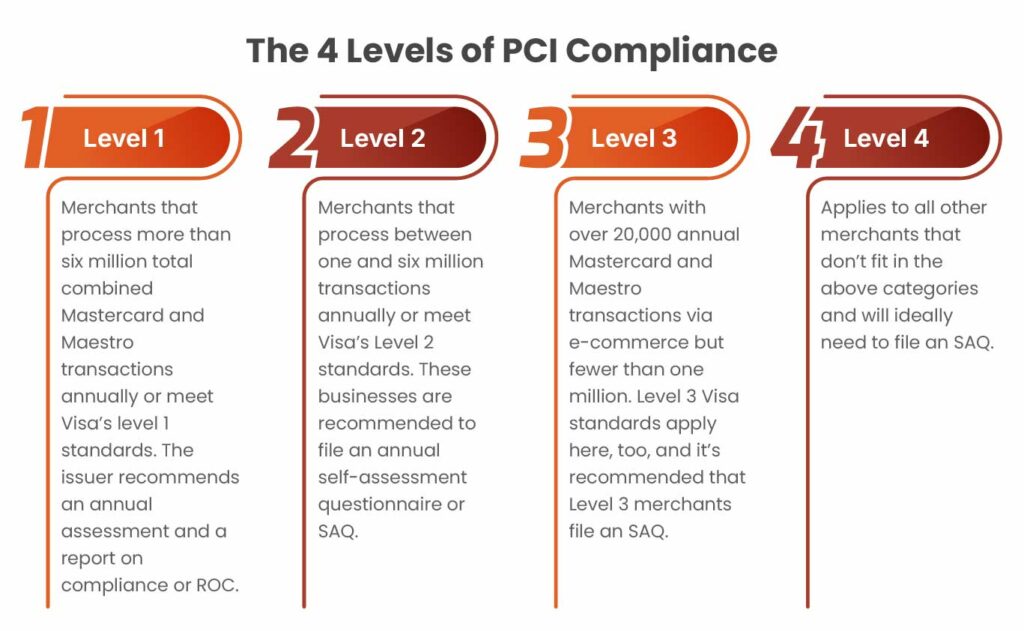

Compliance Levels Under PCI DSS

PCI DSS compliance requirements vary depending on the volume of transactions processed annually.

Merchants are classified into four levels:

Service providers also follow similar tiers depending on the number of merchants they support. This risk-based classification helps ensure that organizations with larger payment volumes implement stronger security controls.

Global Adoption Challenges of PCI DSS Compliance

PCI DSS is global – applicable wherever card payments are accepted – but implementation can vary by region and industry. Large enterprises in North America and Europe typically have rigorous PCI programs, often driven by card brand enforcement and regulatory support. In other regions, awareness and resources may lag. For example, emerging markets may have fewer qualified assessors or less formal oversight, making compliance harder. Small merchants worldwide often struggle with the complexity and cost of PCI audits. Cloud services and emerging payment methods add further complexity: organizations must ensure that their use of cloud platforms or third-party payment apps does not inadvertently broaden PCI scope.

Best Practices of PCI DSS Compliance

Achieving PCI DSS compliance requires organizations to implement strong technical and operational controls across their payment environments. Since payment infrastructures often involve multiple systems, networks, and third-party integrations, organizations must follow structured security practices to protect cardholder data and maintain continuous compliance.

Below are some best practices that organizations should follow to strengthen their PCI DSS compliance posture.

- Minimize Card Data Storage

Organizations should avoid storing cardholder data unless it is absolutely necessary for business operations. Sensitive authentication data such as CVV numbers, PINs, and magnetic stripe information should never be stored after transaction authorization. By minimizing data storage, organizations significantly reduce the scope of the Cardholder Data Environment (CDE) and lower the risk of data exposure during cyberattacks. Techniques such as tokenization and payment gateway integrations can help eliminate the need to store sensitive payment data internally.

- Use Strong Encryption

Encryption is one of the most critical controls required under PCI DSS. Organizations must encrypt cardholder data both at rest and in transit to ensure that the information cannot be read even if it is intercepted by attackers. Strong encryption protocols such as TLS should be used for data transmission across networks, while robust encryption algorithms should protect stored data in databases and backup systems. Proper encryption key management practices must also be implemented to prevent unauthorized access to encrypted data.

- Implement Network Segmentation

Network segmentation helps isolate the cardholder data environment from the rest of the organization’s IT infrastructure. By separating payment systems from other corporate networks, organizations can significantly reduce the attack surface and limit the scope of potential breaches. If an attacker gains access to another part of the network, segmentation prevents them from easily reaching systems that store or process cardholder data. This practice also simplifies compliance efforts by reducing the number of systems that fall under PCI DSS requirements.

- Monitor Payment Systems Continuously

Continuous monitoring is critical for detecting suspicious activities and potential security incidents. Organizations should implement centralized logging and monitoring solutions, such as SIEM platforms, to collect and analyze logs from payment systems, servers, and network devices for effective security monitoring. Real-time monitoring enables security teams to identify abnormal behaviors such as unauthorized access attempts, unusual transaction patterns, or system anomalies. Early detection of these activities helps organizations respond quickly and prevent potential data breaches.

Book Your Free Cybersecurity Consultation Today!

How Kratikal Can Help You with PCI DSS Compliance?

Kratikal provides end-to-end support to help organizations achieve and maintain Payment Card Industry Data Security Standard by combining compliance expertise with practical cybersecurity implementation. The process begins with a comprehensive gap and scope assessment, where experts identify systems that store, process, or transmit cardholder data and evaluate existing controls against the 12 PCI DSS requirements. Based on this assessment, Kratikal develops a detailed remediation roadmap and assists organizations in implementing necessary security controls, policies, and procedures to close compliance gaps. Additionally, Kratikal provides continuous compliance support through the final Qualified Security Assessor (QSA) audit, ensuring that organizations successfully validate their compliance and receive the official Report on Compliance (RoC). This structured approach helps businesses strengthen their payment security posture while meeting global PCI DSS standards.

FAQs

- What is the PCI DSS compliance checklist?

The assessment stage begins with identifying where cardholder data exists within the organization and creating an inventory of IT assets and systems involved in payment card processing. It then involves evaluating these systems and business processes to identify potential security vulnerabilities.

- Why is PCI DSS compliance important for organizations?

PCI DSS compliance is important because businesses that store or process customer credit card data must ensure that this information is properly protected. Without adequate security measures, organizations may expose customers to fraudulent attacks and financial institutions to significant financial losses.

- Is PCI DSS compliance mandatory?

PCI DSS compliance is required for any organization that processes, stores, or transmits payment card data. It helps protect cardholder information and reduces the risk of data breaches.

- How does PCI DSS compliance affect e-commerce businesses and online retailers?

For e-commerce businesses and online retailers, PCI DSS compliance plays a critical role in securing payment card data. Adhering to these requirements helps protect sensitive customer information and strengthens customer trust. Non-compliance increases the risk of data breaches, financial penalties, and damage to brand reputation.

Leave a comment

Your email address will not be published. Required fields are marked *